World-Class Tin Projects with Global Impact

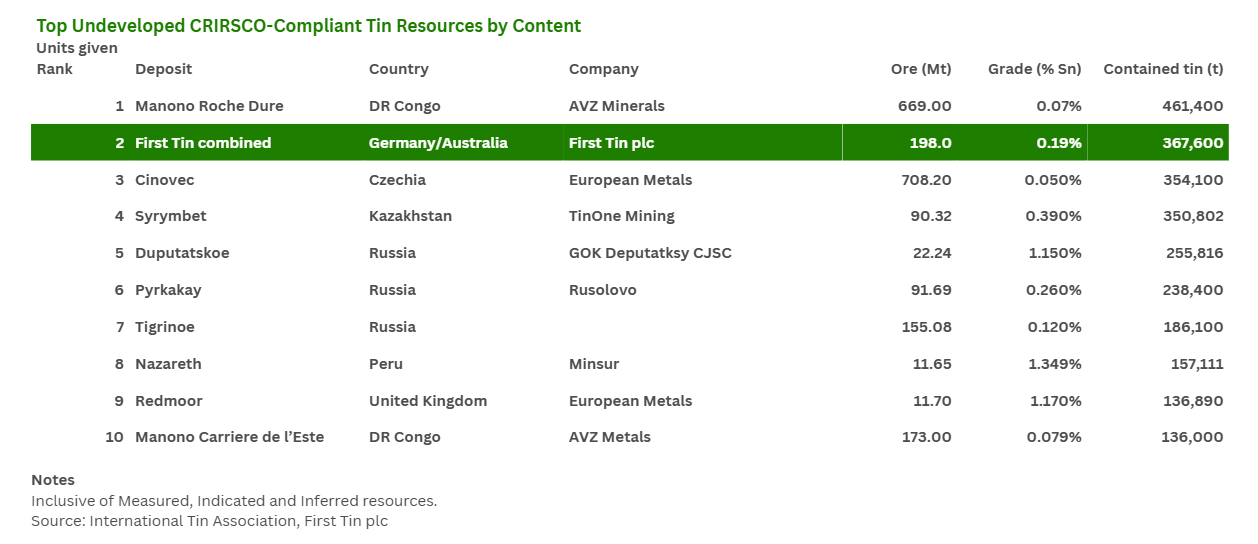

First Tin’s Australian and German tin assets have a clear value-accretive path to producing up to 10,000 tonnes of tin annually. With over 368,000t of contained tin, we have the world’s 2nd largest undeveloped tin resources, outside China.

Both assets are ideally located in conflict-free OECD jurisdictions with established infrastructure and regulatory frameworks from a long history of mining. With established reserves and simple mineralogy, these projects offer a quick route to production, backed by active licenses.

But we care about more than just strategic positioning. We are committed to sustainable, professional, responsible and regulated mining, focused on safety and minimising our footprint, to leave a positive legacy. Our mission is to become a leading global supplier of sustainable tin, meeting the needs of the clean energy, electrification, and technology markets for this critical metal.

(1)")

Taronga – Australia

Acquired in 2022, our Taronga project is located 7km northwest of Emmaville, a historic tin and gem town in the Northern Tablelands of New South Wales, Australia. It lies within a historical tin mining area, with mining, exploration and prospecting dating back to the 1870s and is well positioned to potentially be the world’s next new tin mine.

Tellerhäuser – Germany

Tellerhäuser is located in Saxony’s historic tin district and forms part of our Rittersgrün Mining Licence, valid until 2070. It is one of the most advanced undeveloped tin projects in the world. The Tellerhäuser tin project consists of the Hämmerlein, Dreiberg and Zweibach resources.

The site includes a former GDR mine, and ongoing development is backed by strong technical fundamentals, a polymetallic resource offering by-product credits, and proximity to existing infrastructure, offering a cost-effective route to production.

Gottesberg – Germany

Auersberg – Germany

Compelling Exploration, Ready for Discovery

Adjoining our Tellerhäuser and Gottesberg licences, Auersberg covers 175.7 km² and hosts the largest tin-in-sediment anomaly in Saxony.

This licence presents a compelling opportunity for new discoveries and value creation, especially as part of our now continuous 237.8 km² landholding in the region.

Resources

Germany Mineralisation

Classification | Deposit | Tonnage (Mt) | % Sn | Contained Tin (t) | Notes |

Measured | 0.0 | 0.00 | - | ||

Indicated | Tellerhaeuser | 10.0 | 0.45 | 45,000 | 1,2,6 |

Gottesberg | 6.1 | 0.23 | 14,200 | 1,3,7 | |

Total Measured & Indicated | 16.1 | 0.37 | 59,200 | ||

Inferred | Tellerhaeuser | 18.0 | 0.52 | 93,600 | 1,2,6 |

Gottesberg | 31.1 | 0.25 | 77,100 | 1,3,7 | |

Total Inferred | 49.1 | 0.35 | 170,700 | ||

Measured, Indicated and Inferred | Tellerhaeuser | 27.9 | 0.50 | 138,600 | 1,2,6 |

Gottesberg | 37.0 | 0.25 | 90,900 | 1,3,7 | |

Total Measured, Indicated & Inferred | 64.9 | 0.35 | 229,500 |

Australia Mineralisation

Classification | Deposit | Tonnage (Mt) | % Sn | Contained Tin (t) | Notes |

Measured | Taronga | 39.2 | 0.13 | 51,200 | 1,4,8 |

Indicated | Taronga | 46.5 | 0.10 | 46,400 | 1,4,8 |

Total Measured & Indicated | 85.7 | 0.11 | 97,700 | ||

Inferred | Taronga | 46.2 | 0.08 | 38,900 | 1,4,8 |

Total Inferred | 46.2 | 0.08 | 38,900 | ||

Total Measured, Indicated & Inferred | 132.0 | 0.10 | 136,600 |

Total

Classification | Deposit | Tonnage (Mt) | % Sn | Contained Tin (t) | Notes |

Measured | Taronga | 39.2 | 0.13 | 51,200 | 1,4,8 |

Indicated | Taronga | 46.5 | 0.10 | 46,400 | 1,4,8 |

Tellerhaeuser | 10.0 | 0.45 | 45,000 | 1,2,6 | |

Gottesberg | 6.1 | 0.23 | 14,200 | 1,3,7 | |

Total Measured & Indcated | 101.8 | 0.15 | 156,800 | ||

Inferred | Taronga | 46.2 | 0.08 | 38,900 | 1,4,8 |

Tellerhaeuser | 18.0 | 0.52 | 93,600 | 1,2,6 | |

Gottesberg | 31.1 | 0.25 | 77,100 | 1,3,7 | |

Total Inferred | 95.3 | 0.22 | 209,600 | ||

Measured, Indicated & Inferred | Taronga | 132.0 | 0.10 | 136,600 | 1,4,8 |

Tellerhaeuser | 27.9 | 0.50 | 138,600 | 1,2,6 | |

Gottesberg | 37.0 | 0.25 | 90,900 | 1,3,7 | |

Total Measured, Indicated & Inferred | 196.9 | 0.19 | 366,100 |

Reserves

Australia

Classification | Deposit | Tonnage (Mt) | % Sn | Contained Tin (t) | Notes |

Proved | Taronga | 26 | 0.14 | 36,000 | 1,9 |

Probable | Taronga | 13 | 0.12 | 16,000 | |

Proved + Probable | Taronga | 40 | 0.13 | 52,000 |

- Errors may occur due to rounding, all numbers quoted to a level of accuracy deemed by suitable consultants.

- Estimates prepared by DMT, April 2024, reported in accordance with JORC 2012 code and guidelines.

- Estimates prepared by H&S Consultants, October 2025, reported in accordance with JORC 2012 code and guidelines.

- Estimates prepared by H&S Consultants, March 2026, reported in accordance with JORC 2012 code and guidelines.

- Estimates prepared by Australian Mine Design and Development (AMDAD), May 2024, reported in accordance with JORC 2012.

- Cut-off 0.20% Sn.

- Cut-off 0.15% Sn.

- Cut-off 0.05% Sn.

- Estimates prepared by AMDAD, May 2024.